Setting up a limited company in the UK can be a complex process, but it is worth it for the many benefits that it offers. Limited companies have limited liability, which means that the owners are not personally liable for the debts of the business. This can be a major advantage if the business goes bankrupt. Limited companies also benefit from certain tax breaks, such as the ability to offset business expenses against profits.

If you are thinking of setting up a business, a limited company is the best option for you. In this blog, we will discuss all you need to know before setting up a limited company in the UK.

A limited company is a business structure that offers limited liability to its owners, also known as shareholders. A limited company can be either a private or public limited company.

Private Limited Company: A private limited company (LTD) is owned by one or more individuals and has fewer regulations than a public limited company. It is the most common type of business structure in the UK. The owners have personal liability only up to the amount they have invested in the business.

Public Limited Company: A public limited company (PLC) can issue shares on the stock exchange, have more complex financial rules, and require higher levels of disclosure than other companies. PLCs must meet minimum capital requirements set by law and must include ‘plc’ or ‘PLC’ in their names.

To set up a limited company, you must first determine what type of company you want to form. You will need to choose a name for your business and register it with Companies House, the UK government agency responsible for maintaining records of companies in England and Wales.

You will also need to have at least one director and one shareholder who own at least one share each and can be the same person. The shareholders are responsible for appointing directors who will manage the business on their behalf.

You will also need to decide how much money you want to invest in the business and how much authorised capital you want your company to have. Authorised capital refers to the maximum amount of funds that can be raised by issuing shares.

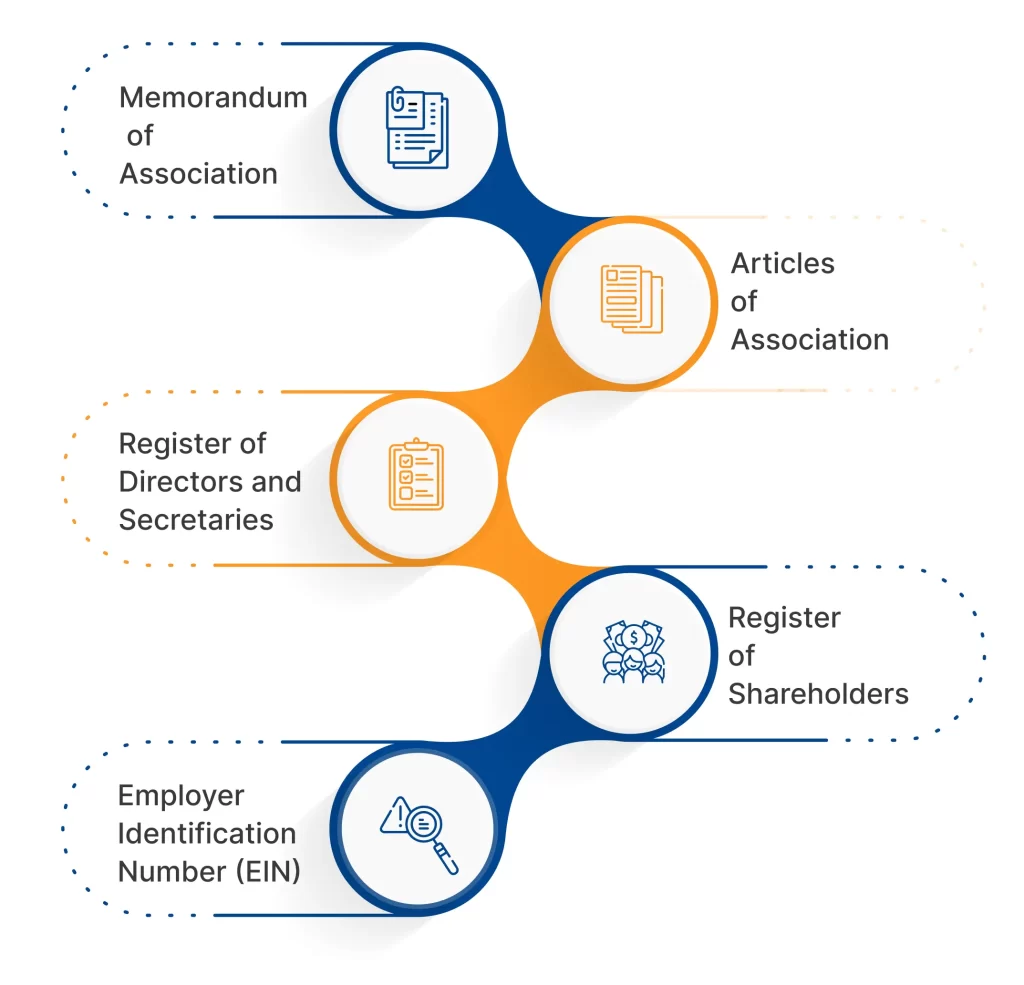

Once you have chosen a name and registered your limited company with Companies House, there are several steps you should take. You will need to set up a bank account for the business and also obtain an employer identification number (EIN) so that you can pay taxes on its income.

In addition, you must decide how your company’s profits will be distributed and how taxes will be paid. You should also draft articles of association, which set out the rules for running your company. These documents must be filed with Companies House along with the relevant fees.

To set up a limited company, you will need the following documents:

To set up a limited company, you must meet certain requirements. Firstly, you must have at least one director and one shareholder of the company. The directors are the people who manage the business and make decisions on behalf of the shareholders.

You will also need to register for Corporation Tax within three months of setting up your company. This will ensure that you pay the correct amount of tax on any profits you make.

Finally, you must also register for Value Added Tax (VAT) if your turnover is more than £85,000 in a 12-month period. This type of business structure is subject to more regulation and filing requirements than other structures, so you should ensure that you understand all the rules before setting up a limited company.

Setting up a limited company comes with many benefits. Firstly, it offers protection to its owners and shareholders as they have personal liability only up to the amount they have invested in the business.

In addition, limited companies can raise funds more easily by issuing shares and can access loans from banks at better rates. They also enjoy lower taxes as dividends are subject to lower tax rates than other forms of income.

The following are also some of the benefits of setting up a limited company:

Finally, limited companies are more attractive to potential investors because of their regulatory structure and the added protection they offer to shareholders.

You will also need to obtain an official stamp for your business, which is used to sign documents relating to the company. Once you have all these documents, you can submit them to Companies House.

When setting up a limited company, you should also consider the differences between public and private companies. A private limited company offers fewer regulations than a public limited company but may not be able to access certain sources of capital.

On the other hand, a public limited company can issue shares on the stock exchange and may have greater access to capital, but it must meet minimum capital requirements and disclose more information to the public.

Ultimately, the type of company you choose should be based on your business needs and goals. However, it is important to note that setting up a limited company requires careful consideration as there are many legal liabilities and regulations involved.

Setting up a limited company comes with both advantages and disadvantages. Private companies are generally more flexible regarding regulations, but they may be unable to access specific sources of capital.

On the other hand, public companies can issue shares on the stock exchange, have more complex financial rules, and require higher levels of disclosure than other types of businesses.

Setting up a limited company can be expensive, but when compared to other types of business structures, the cost is relatively low. Other forms of business, such as sole traders, partnerships, and freelancers, will incur higher start-up costs.

In addition to the initial set-up costs for a limited company, there are also annual costs that must be taken into consideration. These include legal fees, accountancy costs, and audit fees.

However, the long-term benefits of a limited company outweigh these costs significantly. Companies can raise funds more easily by issuing shares and can access loans from banks at better rates. They also enjoy lower taxes and can pass on profits to shareholders without paying income tax.

When setting up a limited company, other considerations must be considered. These include selecting a business name, choosing where to register the company, and appointing directors. It is important to ensure that the name chosen is unique as well as legal and appropriate for your business.

In addition, some regulations must be followed when setting up a limited company. The Companies Act 2006 contains all of the relevant information, and any directors or shareholders should familiarise themselves with this document before making any decisions about the company’s structure.

Finally, it is important to ensure that the right insurance policies are taken out and that all legal requirements are met. Doing so will help to protect the company in case of any disputes or claims.

Overall, setting up a limited company in the UK can be a complex process. However, with the right preparation and research, it is possible to set up a successful business. Careful consideration should be given to deciding between public and private companies as there are advantages and disadvantages to both types of businesses. Ultimately, the decision should depend on your business needs and goals. By following this guide, you can set up a limited company in the UK with greater confidence.